West Ham United’s finances and mounting debt have become a defining storyline for the club’s trajectory, raising critical questions about sustainability amid Premier League pressures. As the Hammers navigate ownership transitions and stadium legacies, understanding their fiscal health reveals both vulnerabilities and strategic pathways forward.

Financial Snapshot

West Ham United reported a staggering net loss before tax of £104.2 million for the year ending May 2025, marking one of the club’s most challenging financial periods in recent memory. This figure stemmed from a 16% revenue decline to approximately £227 million, driven largely by the absence of European competition income that had previously bolstered the books. Despite increased commercial deals and matchday earnings from the London Stadium, operating costs spiraled, with wages rising 9% to push the wage-to-revenue ratio to an precarious 77%.

The club’s amortisation charges—reflecting the annual write-down of player transfer fees—surged 19% to £80.3 million, underscoring heavy squad investment without proportional on-pitch returns. Interest payments alone consumed £21 million, a figure critics have labeled “eyewatering” given the backdrop of stagnant revenues and no major trophies to justify the outlay. These metrics paint a picture of a club living beyond its means, where short-term ambitions have eroded long-term stability.

Historical Debt Evolution

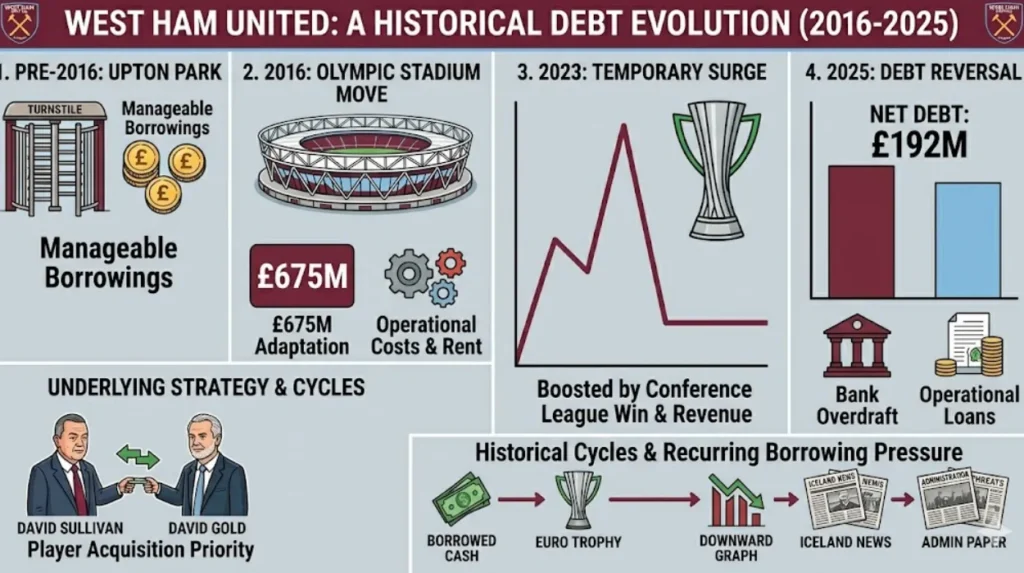

West Ham’s debt profile has evolved dramatically since the move from Upton Park to the Olympic Stadium in 2016, a relocation initially hailed as a revenue boon but later criticized for its fiscal burdens. Pre-stadium, the club carried manageable borrowings, but the £675 million joint venture with Newham Legacy Investments to fund stadium adaptations saddled West Ham with significant long-term liabilities, including annual rent payments exceeding £2.5 million and shared maintenance costs.

By 2023, optimistic reports positioned the club as “essentially debt-free,” crediting revenue surges from the UEFA Europa Conference League triumph and boosted attendances. However, 2025 accounts flipped this narrative, revealing net debt climbing to £192 million, comprising Barclays overdrafts and loans that service ongoing operational needs. This reversal highlights how football’s financial cycles—tied to performance and broadcast deals—can rapidly undo progress, with West Ham’s debt now leveraged against future Premier League distributions.

Ownership under David Sullivan and Daniel Levy has prioritized player acquisitions over debt reduction, a strategy that amplified losses during the 2024/25 season’s mid-table finish. Historic patterns show West Ham repeatedly borrowing to chase European spots, only to face repayment pressures when results falter, a cycle that dates back to the 2000s Icelandic investment debacle resolved via administration threats.

Ownership Influence on Fiscal Strategy

David Sullivan’s stewardship since 2010 has defined West Ham’s financial ethos: pragmatic yet aggressive, blending property magnate savvy with football’s high-stakes gambling. Sullivan, alongside vice-chair Karren Brady, has overseen revenue growth from £50 million pre-takeover to over £200 million annually, fueled by global branding and lucrative sponsorships like the Betway deal. Yet, critics argue this masks reckless spending, with £21 million in interest underscoring over-reliance on loans rather than equity injections.

The 2025 accounts spotlight Sullivan’s reluctance to deploy personal funds, despite Premier League rules permitting up to £100 million in owner loans over three years without FFP penalties. This approach contrasts sharply with rivals like Newcastle, where state-backed investment transformed fortunes. As Sullivan eyes partial divestment amid fan unrest, potential buyers scrutinize the £192 million debt pile, questioning if West Ham’s model can thrive without fresh capital.

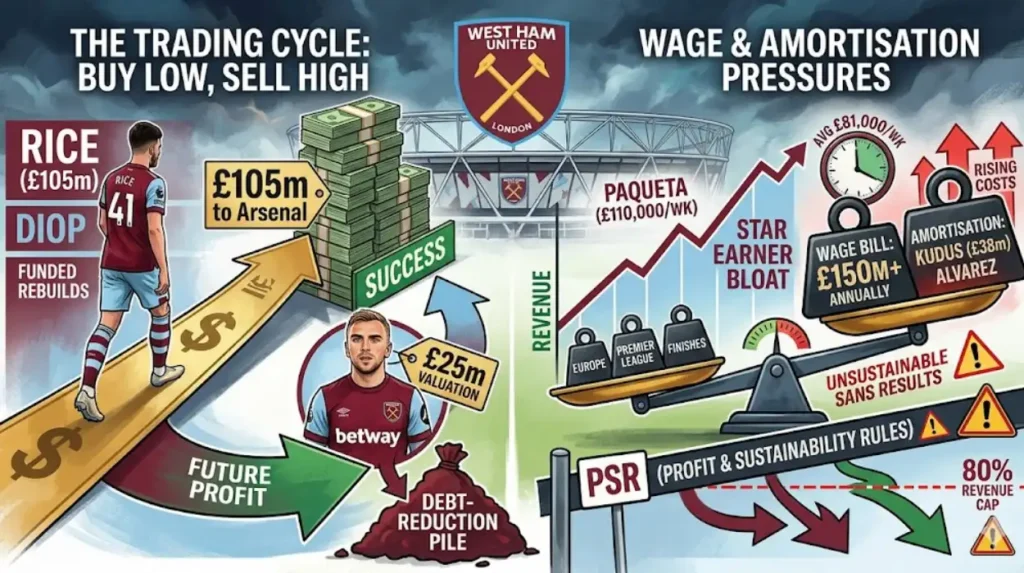

Brady’s commercial acumen has secured deals amplifying non-matchday income, but wage inflation under managers like David Moyes eroded margins. The board’s focus on player trading—selling academy stars like Declan Rice for £100 million—provides cash infusions, yet reinvestment into high-amortisation signings perpetuates the debt loop.

Stadium Legacy Burden

The London Stadium, rebranded Queen Elizabeth Olympic Park, remains West Ham’s financial Achilles’ heel. Secured via a 99-year lease, the venue promised 54,000 capacity and multi-use revenue streams, delivering average attendances near 62,000 and £40 million in annual matchday income. However, transformation costs exceeded £323 million, with West Ham’s share locked into escalating service charges projected at £25 million over the lease term.

Unlike Tottenham’s debt-free stadium model, West Ham’s deal lacks full control, ceding athletics track naming rights and non-football events to Newham Council. This hybrid setup generates ancillary income—concerts by artists like Guns N’ Roses—but pales against rivals’ integrated developments. Debt servicing for stadium adaptations contributes directly to the £192 million figure, with projections warning of rising costs as legacy obligations mature.

Fan discourse frames the stadium as a “white elephant,” its £1.5 million monthly running costs dwarfing Upton Park’s efficiencies. Yet, without it, West Ham’s global appeal—key to £80 million broadcasting revenues—would diminish, tying fiscal health to consistent top-flight status.

Profit and Sustainability Rules Impact

Premier League Profitability and Sustainability Rules (PSR), formerly FFP, loom large over West Ham’s future, capping losses at £105 million over three years. The 2025 £104.2 million deficit edges perilously close to this threshold, especially with trailing years showing cumulative strain. Unlike Everton’s points deductions, West Ham has skirted breaches via player sales, but tightening UEFA squad cost ratios—targeting 70%—demand wage restraint.

Amortisation spikes from signings like Mohammed Kudus and Edson Alvarez accelerate PSR pressures, forcing summer sales to comply. The club’s £203 million projected turnover sans Europe underscores vulnerability; relegation would slash revenues by 40%, triggering PSR Armageddon. Strategic sales, such as potential exits for Jarrod Bowen or Lucas Paqueta, offer breathing room but risk squad erosion.

Long-term, PSR evolution under new financial fair play frameworks prioritizes youth development and infrastructure, areas where West Ham lags. Academy outputs provide PSR credits, yet underinvestment hampers this safety net.

Revenue Streams Breakdown

Commercial revenues hit £60 million in 2025, buoyed by kit supplier New Balance and front-of-shirt sponsor Betway, reflecting Sullivan’s deal-making prowess. Matchday income, the stadium’s silver lining, contributes £50 million, with hospitality packages selling out despite pitch distance complaints. Broadcasting remains the lifeline at £120 million from domestic and international rights, though merit payments dipped post-Europa Conference exit.

Player trading yielded £60 million net spend positivity historically, but 2024/25’s £80.3 million amortisation signals imbalance. Without Champions League allure, West Ham misses £30-50 million upsides rivals enjoy. Diversification into digital media and women’s team growth offers modest buffers, yet overreliance on TV money exposes cyclical risks.

Player Trading and Wage Pressures

West Ham’s transfer market strategy—buy low, sell high—has netted fortunes from Rice (£105 million to Arsenal) and Issa Diop, funding Moyes-era rebuilds. However, incoming fees for Kudus (£38 million) and Alvarez inflate amortisation, with weekly wages averaging £81,000 club-wide. Star earners like Paqueta (£110,000/week) exemplify bloat, pushing the £150 million wage bill unsustainable sans results.

Future trading hinges on Bowen (£25 million valuation) and Fernandes, whose sales could erase debt chunks while funding youth. Yet, agent fees and bonuses compound costs, with PSR demanding amortisation caps below 80% of revenue.

Implications for Club Competitiveness

Debt constrains West Ham’s title aspirations, limiting net spend to £50 million summers versus Manchester United’s billions. Mid-table stasis risks a “vicious cycle”: no Europe means no revenue, breeding poor recruitment and fan apathy. Relegation, though buffered by stadium deals, would invoke administration ghosts, slashing value by £400 million.

Positive levers include Sullivan’s property expertise repurposing training grounds and global tours netting £10 million annually. Women’s team ascent adds soft power, potentially unlocking title sponsorships.

Navigating Debt Toward Stability

Debt reduction demands European qualification, targeting £250 million turnover via top-six finishes. Ownership change—amid 2026 takeover whispers—could inject £200 million equity, mirroring Brighton’s model. Cost-cutting via wage deferrals and non-core asset sales (e.g., training kits) provides interim relief.

PSR compliance via loans-to-equity conversion shields against penalties, while infrastructure credits from stadium upgrades build buffers. Fan ownership initiatives, like share schemes, foster loyalty without fiscal drag.

Strategic Roadmap Ahead

West Ham’s future pivots on 2026/27: Europa League return via cups restores £40 million, stabilizing wages at 65% ratio. Diversify via NFL-style stadium events, aiming £20 million extras. Prioritize data-driven recruitment, halving amortisation through loans and free agents.

Board refresh post-Sullivan emphasizes sustainability, with Levy’s Tottenham blueprint inspiring debt-free ambitions. Academy Class of 2025 talents like George Earthy offer PSR-compliant pathways. Ultimately, prudent stewardship transforms debt from millstone to motivator, positioning West Ham as East London’s enduring powerhouse.