Every generation gets the mania it deserves, and ours has arrived wrapped in silicon. The dot-com crash and the 2008 collapse are the two ghosts now summoned to explain the AI boom. Both comparisons are seductive. Both, I will argue, are wrong, or at least wrong enough to be dangerous. The more interesting question here is not whether this ends in tears, but who is crying when it does, and what they were standing next to when the water started rising.

If you’ve been online recently you must have seen countless posts fear-mongering about an AI bubble. But the truth is you cannot judge a bubble from inside it. That is the first thing history teaches, and it is the most inconvenient, because by the time the verdict is obvious the money has already been made or lost. So, we do the next best thing. We reach for the past, hold it up against the present, and squint. The trouble is we tend to reach for the wrong bit of the past, and we squint at the parts that flatter whatever we already believed. As the saying goes,

“Those that fail to learn from history are doomed to repeat it.”

Let me declare my hand at the start, because that shapes everything that follows. I personally do not believe we are in an AI bubble, or at least not the kind that ends the way 2000 and 2008 ended. I believe that AI is being underestimated rather than over hyped by the vast majority, and that current prices, stretched as some of them clearly are, are closer to fair than the doom-mongers will allow. I could be wrong. People who were certain about this back in 1999 were also intelligent, also well informed, and early to a party that ended up being a funeral. So, take the conviction with the appropriate seasoning. But conviction it is.

The Dot-Com bubble: What Actually Happened

The dot-com bubble is remembered as a morality tale about stupidity, which is unfair, and which obscures the mechanism. The internet was real, that was never the delusion. The delusion was timing, and arithmetic, and the belief that adoption would arrive on the same schedule as the share price.

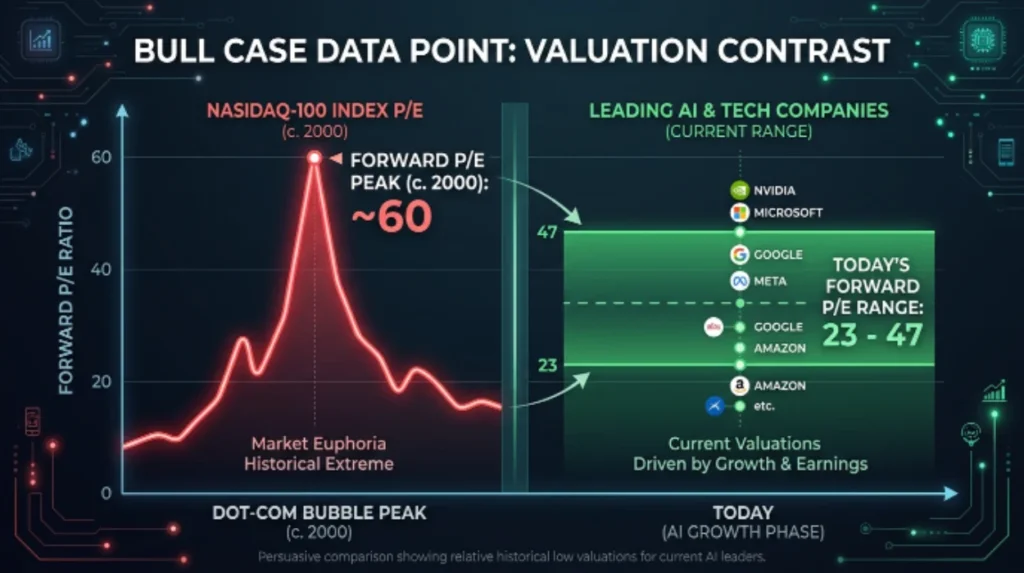

Here is the part that matters for our purposes. At its peak in March 2000, the Nasdaq100 traded on a forward price-to-earnings ratio of around 60. Roughly one in seven dot- com companies were actually profitable. The financing had a circular quality that ought to sound familiar: internet firms bought equipment from Cisco, Cisco’s revenue soared on the strength of it, this soaring revenue justified Cisco’s inflated valuation, and that valuation underwrote yet more confidence in the whole edifice. Telecoms laid fibre on borrowed money against demand forecasts that assumed the future would arrive on your average Tuesday afternoon. When it did not, the leverage did what the leverage always does. Cisco lost roughly 90% of its value. Amazon fell 93% from its 1999 high, then went on to become one of the most valuable companies in human history.

Read that last sentence again, because it is the whole lesson compressed. Identifying the right technology was necessary and nowhere near sufficient. You could have been completely correct about the internet and still been ruined by the timing. Valuation and patience were the entire game, and almost nobody had enough of either.

The 2008 Financial Crisis: What Actually Happened

2008 was not 2000 in a different outfit. It was a fundamentally different animal, and conflating the two is the analytical sin underneath most of the lazy bubble commentary. The dot-com crash was an equity story: overvalued shares fell, paper wealth evaporated, the damage was largely contained to people who owned the shares. Painful, but bounded.

2008 was a debt story, and debt is where the real damage lives. The asset at the centre, American housing, was not even especially overvalued by the standards of a tech mania. What made it lethal was the leverage stacked on top, the derivatives stacked on the leverage, and the fact that the entire global banking system had quietly agreed to treat the riskiest tranches as safe. When the housing assumption broke, the leverage transmitted the failure everywhere at once. This is the distinction that matters: an equity bubble bursting makes shareholders poor; a debt bursting bubble makes everyone poorer, because the financial plumbing itself collapses.

Which brings me, unavoidably, to The Big Short, the film every finance writer is now contractually obliged to mention at least once. If you remember Christian Bale building his thesis in a darkened office while everyone called him mad, you remember the seductive part: that once clever contrarian saw it coming. What the film glosses, because it makes for worse cinema, is that being right and being early are nearly indistinguishable until the very end, and most of the people who ‘saw it coming’ back in 2006 were carried out on stretchers in 2007 before their thesis paid off. The lesson Hollywood sold was ‘trust the lonely genius’. The lesson the market actually teaches is ‘the genius nearly went bust waiting.’ Michael Burry, the real one, is back in 2026 warning that AI looks like the late innings of dot-com. He may be right again. He was also early enough, last time, that it nearly killed the trade before it worked out. File that.

So Which Ghost Is Haunting Us?

The bubble case for AI is not stupid, and I am not going to insult you by pretending that it is. The strongest version goes roughly like this. Market concentration is at levels not seen since the dot-com era, with AI related names having driven something like 80% of the S&P 500’s gains in 2025. The financing has gone circular in a way that genuinely rhymes with 1999: Nvidia commits up to $100 billion to OpenAI, which spends it on Nvidia chips; Nvidia takes a stake in CoreWeave through to 2032; Microsoft owns a quarter of OpenAI and supplies the cloud that OpenAI’s revenue partly flows back to pay for. Harvard’s Andy Wu puts it with lethal economy: in some cases it looks like Nvidia is effectively paying its customers to buy its products. And so far the returns are thin on the ground. An MIT study found that 95% of enterprise generative-AI projects were producing no measurable return. The dollars circulate; the demand they imply may be partly an accounting echo.

That is a serious case. I want to give it its full weight before I explain why I still do not buy it as a 2000 or 2008 analogue.

Now the other side, Nvidia trades around 47x earnings, which is rich, but it is not the 60 times forward with no profits insanity of the Nasdaq in 2000. The companies at the centre of this boom make actual money: Nvidia posted $215.9 billion in revenue in its 2026 financial year, up 65%. Corporate cash flow across the big spenders is, by Morgan Stanley’s reckoning, roughly triple its 1999 level, which means the capital expenditure, vast as it is, is being funded substantially from earnings rather than purely from debt. AI capital spending is now running at around 0.8% of US GDP, which sounds enormous until you learn that comparable technology booms over the past 150 years peaked closer to 1.5%. Even Jerome Powell, not a man given to ramping markets, has drawn the distinction explicitly: these firms generate real revenue and real output, which is precisely what the dot-com darlings did not.

Here is my actual position. The thing that people keep calling a bubble is mostly the financing structure, not the technology and not the underlying demand. The circular deals are a real risk, the most real one, and if AI is going to break something it will break there, in the private-credit funded data-centre loops where leverage hides from public scrutiny. But that is a containable, identifiable fault line, not a mispricing of the entire asset class. Bezos called this an ‘industrial bubble,’ and I see that as the most honest framing available: capital will be wasted, individual companies will detonate, and society will still inherit the infrastructure on the other side. The Internet was worth building even though pets.com was not.

The Man Who Calls Doubt ‘Blasphemy’

Days ago, at SoftBank’s annual meeting in Tokyo, Masayoshi Son told shareholders that calling AI a bubble is ‘blasphemy against AI.’ It is just the beginning, he said. The potential is barely unlocked. He intends to keep going into his seventies, chasing what he calls artificial super intelligence, having compared SoftBank, not for the first time, to a goose that lays golden eggs.

You should take Son seriously and not literally, and the distinction is the whole point. Here is a man who has actually traded through full cycles, the dot-com boom and its bust, the COVID crash that dumped his portfolio into what he cheerfully called ‘Corona Valley.’ That is real scar tissue, and scar tissue is worth listening to. But notice the tell. ‘Blasphemy’ is the language of faith, not analysis, and Son is not a neutral observer of the AI trade. He is the most leveraged believer on the planet, having committed around $65 billion to OpenAI alone, even straining SoftBank’s borrowing limits to do so. When the largest holder of a position tells you that doubting the position is heresy, you have learned a great deal about his conviction and almost nothing that you can put into a valuation model. Is he early, or is he too close to the trade to call it? My read: he is genuinely right about the technology and an unreliable witness on the price, and those two things can comfortably coexist. The goose may well lay golden eggs. That does not tell you what to pay for the goose.

The East London Footnote That Is Not a Footnote

All of this can feel very far from home, a story about Tokyo boardrooms and Californian chip designers. It is not. When market concentration reaches the level it has now, a correction in five or six American stocks does not stay there. It travels, through index funds, through the pension allocations of West Midlands council workers, through the Scottish Mortgage holdings sitting in ISAs across Newham and Tower Hamlets. The boroughs of East London own a slice of this trade whether or not anyone living in them has heard of CoreWeave. If the circular financing unwinds, the loss does not announce itself as ‘AI exposure’ on anyone’s statement. It just shows up as a smaller pension.

There is a second, slower connection, and it matters more. The data centres powering this boom are landing in and around this city, pushing east into the Docklands and Essex, and they consume two things in enormous quantity: electricity and capital. Both are being diverted towards compute and away from other uses, including, as I have written before, housing that now waits years for a grid connection. The AI build-out is not an abstraction in East London. It is a physical competitor for the same finite resources the area was already short of.

Which Is Where the Heat Comes In

As I write this, Britain is in the middle of a red extreme-heat warning. On Thursday the temperature hit 36.7C at Merryfield in Somerset, the hottest June day the country has ever recorded, beating a record that had stood for less than twenty-four hours. The Met Office did not hedge: this is, in its chief meteorologist’s words, further evidence of how high-temperature extremes are becoming more common as a result of human induced climate change.

And this is the part where I stop being an analyst and admit to a stake. I do not want AI to be stopped; I think it is becoming the pinnacle of human innovation, and I predict the people forecasting its collapse are mostly wrong. But useful is not the same as harmless, and the bill for the harm is being quietly socialised, onto the grid, onto the housing queue, onto the atmosphere, while the gains concentrate in a handful of balance sheets that recycle money between each other and call it growth. The green economy has shown us that capital can be pointed at the climate problem when the incentives are built right. The same discipline has not yet been pointed at AI’s energy footprint, and there is no good reason it cannot be, beyond the fact that nobody with the power to do it currently has to.

So here is where I land, holding it loosely, the way you should hold any forecast made from inside the weather. We are probably not in a bubble that bursts like 2000 or 2008 does, because the revenue is real, the funding is mostly earnings-backed, and the leverage, while it has crept into the financing loops, has not yet metastasised through the banking system the way subprime did, there will be a correction. Corrections this concentrated are close to a mathematical certainty, and I would not be surprised by a 20 to 30% rest in the most stretched names. The technology survives it. The weakest financing structures do not. That is healthy, not catastrophic.

The part I would actually lose sleep over is not the share price, rather, it is that we build all of this, brilliantly, expensively and forget to make it clean while we still have the cheap capital and the political attention to do it. This heat wave will pass. The next one will be hotter. We have, at most, a narrow window in which the AI boom and the climate emergency can be made to solve each other rather than compound each other, and windows like that do not stay open very long. Build the future. Just do not cook the planet to power it. We have learned, twice now, what happens when we let the financing get ahead of the reality. The lesson was never that the technology was fake. It was that we noticed the cost too late.